How to figure out actual returns in today’s commercial property market

Often when yields are reported there’s no clarification on what kind of yields are being referred to, which can be misleading to investors who are unfamiliar with the market. In turn, they’re not able to calculate accurate returns.

Sometimes you may find that an agent would refer to the Cap Rate almost like a price point, and when they refer to yields, they may be talking about initial yield (passing net income divided by purchase price) or equivalent yield (weighted average yield) or equivalent for a Cap Rate, or they could be quoting it on passing as opposed to market. It’s easy to see why the market can be benchmarked incorrectly at times.

The most quoted yield is the ‘initial yield’ which can also be called ‘passing yield’, which is what the current tenants are paying versus the purchase price. Most people tend to drift towards the initial passing approach, but in Australia, that has dropped away. The market cap approach is deemed a much better view of comparable assets. It is important to use the yield that would accurately reflect the real return of the building you are purchasing, and this is often the market yield, as it includes adjustments that would have been evaluated by a valuer.

So how does the Cap Rate come into play?

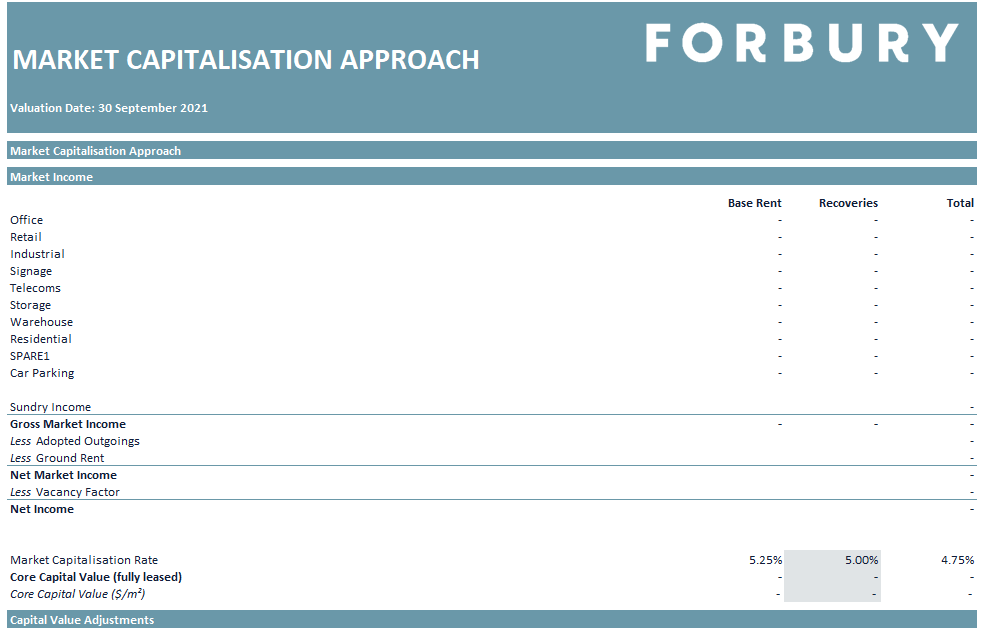

Sometimes when you are buying a simple asset, you may be quoted a Cap Rate, essentially a rate from dividing the net passing income rate by an estimate of what the building is worth. The actual value is calculated from the Core Capital Value with a number of adjustments that bridge the two values, these are called Capital Value adjustments.

In Forbury, these are the below the line or Core Capital Value adjustments. You have your:

Market income

Ground rent (if any)

Outgoings

Vacancy

The Net Income after these adjustments provides the Net Income to Capitalise with the outcome being the Core Capital Value.

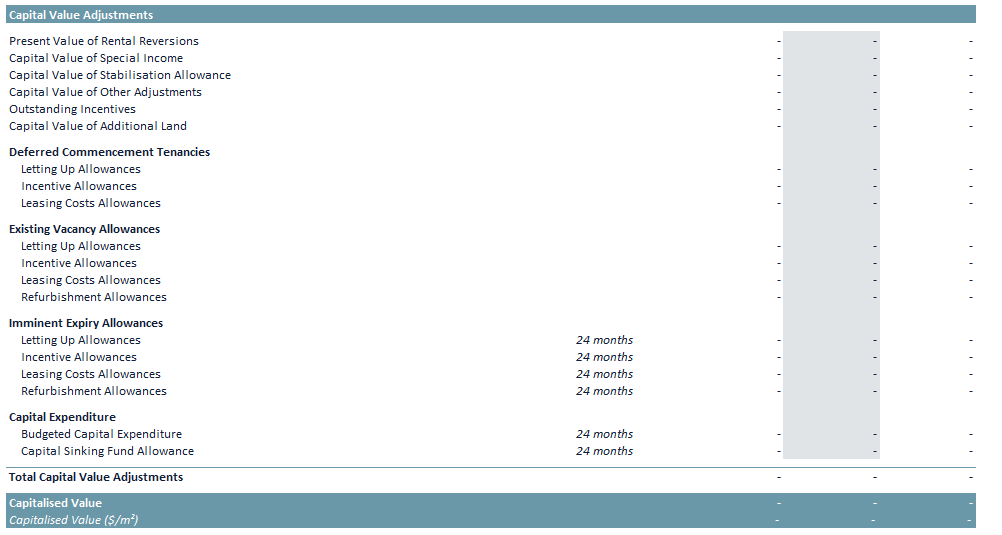

In addition, there are Capital Value Adjustments, such as:

Other and special income

Deferred Commencement Tenancies

Existing Vacancy Allowances

Imminent Expiry Allowances

Capital Expenditure

Combining both the Core Capital value and the Capital Value adjustments aid in determining what a purchaser is likely to pay to acquire the property.

What adjustments need to be made?

Many adjustments occur when you’ve got vacant tenants, therefore the rental reversion figure is a key figure to look at when making below-the-line adjustments. If the market rent is the same as the passing rent, then you would get the same figure for your above the line Cap Rate, but if the market rent is not the same as the passing rent, and you have the same Cap Rate, you can make an adjustment below the line with the rental reversion figure making up the number you are capping.

If the passing rent is lower than the market rent, then you will be missing out on some income until there is a review which usually happens when a tenant vacates. When there is a renewal, the rent is usually increased to match the market rent. When this happens, you must make a deduction for the rental reversions, which takes away the amount of income from what you have capped.

Another way of looking at it is all the capital adjustments below the line. If we look at the CapEx (Capital Expenditure or Capital Expense: money a company spends to buy, maintain, or fix the asset), for example, there is $27 million of CapEx that needs to be spent over the next 36 months, so you would want to deduct that off the value that you are purchasing because the above the line assumes that you own this asset in perpetuity.

If there are tenants that are going to expire within the near term, you need to make an allowance of cash flow hits to get new tenants and because there's also uncertainty on whether you will get new tenants.

Another allowance you could make is if some of the spaces were vacant, if there is a period of say six months before somebody comes in, we may need to give them an incentive, which will incur some costs, or Refurb to refit the space for them.

These make up the below-the-line adjustments, which can have a big or little to no impact on the valuation.

It’s all a balancing act…

The way you adjust for whether a building is superior or inferior, you have got two levers; your Cap Rate and the below the line adjustments, which is a bit of a balancing act.

For instance, you could look at going out to 36 months, and your imminent expires can have a softer Cap Rate, or you can go to 24 months and have a tighter Cap Rate, which is a balancing act of what you want to explicitly assume that needs to be done, versus what you want to assume as a risk, which is reflected in the Cap Rate.

A brand-new industrial property that had blue-chip tenants in it has been sold for $203 million with a 3.3% market Cap Rate vs a decrepit industrial shed that was sold for a 6.35% market Cap Rate and needed $50,000 of CapEx spent. There are two ways to go about it, you can factor in their own refurb or CapEx costs into the market Cap Rate by pushing it up, or you can keep it at a comparable rate, and do it all below the line.

In our Forbury software, you can also add in the capital value of additional land below the line, and these are all assumptions that need to be made using our software, to give the closest or most accurate figure.

ABOUT FORBURY

Over the years, more features and functionality have progressively been added into Forbury's software. We are continuously thinking of better ways to leverage our property valuation tech for the benefit of our customers. Property professionals using Forbury gain increased accuracy and speed, empowering them to cover more of the market without additional resources and expense.

Want to be notified of our new and relevant CRE content, articles and events?

Authors

Jesse Bennett

Product Manager

Authors

Jesse Bennett

Product Manager